Eight Lessons from Australia's First Year of Mandatory Climate Reporting for Mining Companies

- 15 minutes ago

- 4 min read

by Brendan Tapley, Managing Director DECARBONATE

Australia's mandatory climate disclosure regime under ASRS S2 is completing its first reporting cycle for many large organisations. In total, there are an estimated 600 mining and METS companies expected to be captured by the regulation.

The first wave of disclosures has provided several important lessons for companies in the mining sector.

1. Simplifying the disclosures to tell a story

One of the challenges emerging from the first year of ASRS S2 reporting is balancing technical compliance with effective communication. The most effective reporters are increasingly moving beyond simply complying with disclosure requirements and are using climate reporting to tell a coherent business story. This means explaining how climate-related risks and opportunities could affect the organisation, what management is doing in response, and how these issues influence future strategy and decision-making. Clear, concise and well-structured disclosures are often more valuable than lengthy technical reports, provided they remain supported by robust evidence and analysis.

2. Greenwashing is more common than you would think, and business leaders are on the hook

In my experience, as both, an auditor and preparer of sustainability report and climate disclosures, misstatements leading to greenwashing is common. Often it is unintentional and simply due to a lack of controls, systems and general maturity with preparing the subject matter. However, the implications can be serious. ASIC has now executed a handful of greenwashing civil penalty cases, related to a breach of a trustee's duty to exercise care and diligence. And major entities, including Energy Australia, have faced legal challenges targeting consumer products marketed as "carbon neutral," exposing the risk of relying on questionable carbon offset schemes. The ACCC’s review of the sustainability claims of 247 businesses found that 57% made concerning or unsubstantiated claims.

Some companies rely on third party assurance/audit, but greenwashing risks often extends beyond the scope of such an audit. We see this particularly with reporting on progress with climate targets and incentives. For most mining companies – their priorities are mining production targets, revenue and share price; which is prioritised well above the monitoring of emissions and honoring of emissions targets. However, Company Directors are now required to sign-off on the mandatory climate disclosures – meaning that business leaders are on the hook for what is stated in the disclosures. A preventative measure is pre-assurance checks and gap assessments can be effective in identifying material misstatements early in the process.

3. Climate risk is now a financial risk, requiring financial literacy and engagement with key stakeholders

Climate risk is increasingly being treated as a core business and financial risk - linked to asset values, operating costs, project economics, capital allocation decisions and long-term business resilience. For the mining companies that we’re helping to prepare climate disclosures, it’s often the finance teams (if not the sustainability teams) who have the internal responsibility for the climate disclosures. Stakeholder engagement with functions such as Finance, Procurement (on scope 3 emissions), Operations, broader Management and Executive Directors is crucial for preparing disclosures that are accurate, complete and socialised for internal approval.

4. Materiality remains one of the biggest challenges

Many organisations have found it difficult to determine which climate-related risks and opportunities are genuinely material. A point of confusion amongst reporting companies is the definition of ‘materiality’.

ASRS S2 does not seek to identify material risks and opportunities, then disclose them.

Instead, it says:

Step 1:

| Identify climate-related risks and opportunities that could reasonably be expected to affect the entity's prospects (such as prospects for cash flows, access to finance, or cost of capital). |

Step 2: | Determine what information about those risks and opportunities is material and therefore must be disclosed. |

Step 3: | Document an audit trail - why information is included, excluded or prioritised; and evidence, methodologies and governance supporting decisions. |

Defensible materiality assessments are becoming essential, particularly where companies need to justify to financial auditors why certain risks have been included, excluded or prioritised.

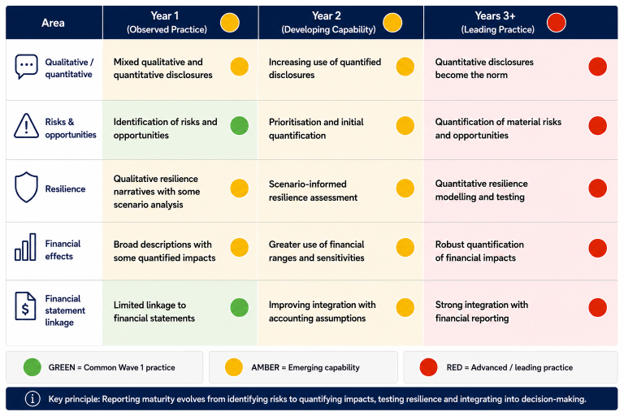

5. ASRS S2 clearly points toward increasing quantification over time

Many first-year reporters relied heavily on qualitative disclosures due to uncertainty and data limitations. However, the ASRS S2 standard does not permit an entity to indefinitely rely on generic qualitative disclosures simply because climate impacts are uncertain.

Regulators and assurance providers increasingly expect organisations to quantify potential financial impacts, undertake scenario analysis and clearly explain assumptions.

What we’re actually seeing in Year 1, and the increasing expectation for quantification of climate related risks and opportunities:

.

Source: Decarbonate 2026, considering Deloitte’s 2026, Early insights into Wave 1 of Australian climate reporting

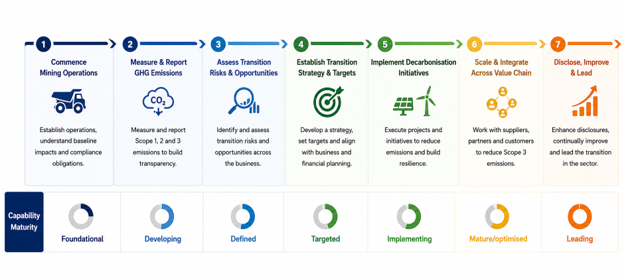

6. Transition risk extends well beyond carbon pricing

Mining companies often focus on carbon regulations for their transition risks. However, increasingly important drivers of business risk and opportunity includes customer expectations, access to finance, technological change, government policy, market competitiveness and supply chain requirements.

Steps to developing more capability to address climate transition risks

Source: Decarbonate 2026

7. Scope 3 emissions are creating value chain pressure

Many organisations that are not directly captured by ASRS S2 are still being affected through customer and investor expectations. Mining companies, contractors and METS businesses are increasingly being asked to provide emissions data and demonstrate climate risk management capabilities. In the first year of reporting, all entities reported Scope 1 and 2 emissions, and 40% voluntarily disclosed Scope 3 emissions despite the opportunity for first-year relief. A majority disclosed climate-related targets, reflecting some maturity in emissions transition planning.

8. Assurance readiness is becoming critical

The focus is now shifting from simply producing disclosures to producing disclosures that can withstand assurance.

Robust governance, reliable data systems, documented methodologies and clear decision-making processes are becoming essential foundations for future reporting.

For mining companies, ASRS S2 should not be viewed solely as a compliance obligation. The organisations that use climate reporting to strengthen governance, improve decision-making and better understand future risks and opportunities are likely to be best positioned in an increasingly competitive and carbon-conscious global market.

Stage | Focus | Outcome |

1 | Compliance | Meet minimum ASRS S2 requirements |

2 | Data & Controls | Reliable emissions and climate data |

3 | Assurance Ready | Robust governance, methodologies and evidence |

4 | Decision Support | Climate insights embedded in investment and operational decisions |

5 | Strategic Advantage | Better understanding of future risks and opportunities |

6 | Market Leadership | Stronger resilience, access to capital and competitive positioning |

About the Author:

Brendan Tapley is Managing Director of Decarbonate, a consultancy focused on climate risk and ESG advisory services in the mining sector. He is one of three people in Australia to sit on the Global Reporting Initiative (GRI) mining sector standard working group. Decarbonate are also GRI training partners on sustainability and ASRS S2 mandatory climate reporting.

Comments